Political uncertainty in the UK comes at an inopportune time, with bond yields rising globally as the disruption in the Gulf continues.

It was all supposed to be so different. When Labour won the 2024 election, many cheered the return of ‘sensible’ politics. However, a shallow majority and a lack of any vision beyond not being the Conservatives has resulted in the prospect of our sixth PM in the last decade. Whatever the outcome of the by-election and the leadership battle, they are unlikely to promote fiscally responsible policies, seeing as the external threats to Labour are from the populist Reform and Green parties.

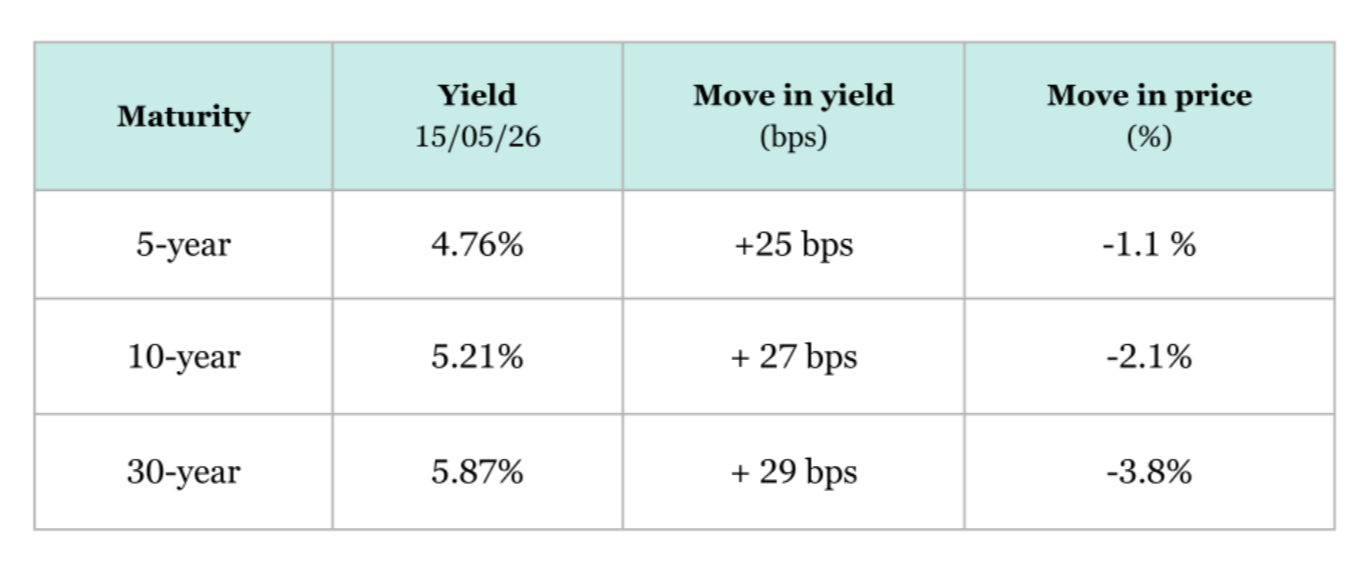

Gilt market action supports cautious stance

The Gilt market reacted to the disruption in the government as expected with yields moving higher along the length of the yield curve. While the move in yields was similar along the curve, the changes in price were not. The longer-dated a bond is, the more sensitive the price is to a move in yield, known as duration. As yields move inversely to prices this meant that the 30-year dropped -3.8% in price terms last week versus the 10-year falling -2.1% and the 5-year falling -1.1%.

For some time, we have felt that the slightly higher yields on offer in longer-dated bonds are not commensurate to the levels of volatility that they provide. Duration in our Tenax Fund is currently 2.6 helped by our allocation of 12.7% to floating-rate notes.

Of course, it is not just the machinations within the Labour party that have caused Gilt yields to increase in recent weeks. And it is not just the UK bond market showing signs of strain.

The conflict in Iran remains unresolved and the Straits of Hormuz are still closed. The disruption to the global economy is yet to fully show up in inflation and economic data, but it surely will. And the longer it takes to find a resolution, the greater the risk will be of higher inflation and lower growth later in the year.

Equities ignoring the warning signals for now

The average 10-year yield for G7 countries is the highest since 2004. If this is a warning signal from the bond market about the prospect of higher interest rates and cost of borrowing in the future, it is not one that the equity market is heeding. US equity markets have risen back up above all-time highs driven by the AI trade and demand for semiconductor chips.

Undoubtedly technology stocks are less vulnerable to the iniquities of inflation, especially when there is a spending race afoot to dominate a new industry. Momentum, however, works both ways. The same forces that have driven the technology sector to such heights can be just as powerful in reverse. After all, the Nasdaq fell -33% in 2022 after the covid-era highs of 2021, while the boring old FTSE rose +1%.

We do not believe we are in a repeat of the inflationary spike of 2022, nor are we in a re-run of the dot-com boom and subsequent bust of 1999/2000. But there are elements of both those periods that are recognisable today, and we feel that it pays to remain cautious.

The above article has been prepared for investment professionals. Any other readers should note this content does not constitute advice or a solicitation to buy, sell, or hold any investment. We strongly recommend speaking to an investment adviser before taking any action based on the information contained in this article.

Please also note that the value of investments and the income you get from them may fall as well as rise, and there is no certainty that you will get back the amount of your original investment. You should also be aware that past performance may not be a reliable guide to future performance.

How would you like to share this?